While Not the Whole Shebang, Forgiving $20,000 in Student Debt is a Major Step in the Right Direction

An educated populace makes for a more productive, prosperous society, and people shouldn't be punished for trying to be a part of it.

When campaigning for the presidency, Joe Biden stated:

“I propose to forgive all undergraduate tuition-related federal student debt from two- and four-year public colleges and universities for debt-holders earning up to $125,000, with appropriate phase-outs to avoid a cliff.”

Still riding the win from the passage of the Inflation Reduction Act, President Joe Biden scored another this week when he signed an executive order authorizing the federal government to cancel up to $20,000 in student debt.

While this frustratingly is not “all undergraduate tuition-related federal student debt” he promised when vying for the White House two years ago, it is nonetheless a major progressive move three months before one of the most consequential mid-term elections in the nation’s history.

There is lots of confusing minutia around this decision, and neither side is short on the inevitable punditry.

But, in short, here is what the student debt forgiveness plan entails, as Business Insider reported:

“Pell Grant recipients making under $125,000 a year will be eligible for up to $20,000 in debt relief.

“All other federal borrowers making under $125,000 a year can get up to $10,000 in loan forgiveness.”

Moreover, Biden paused loan repayment again “for the final time” one week before the looming deadline.

According to a White House fact sheet, the Department of Education will:

“Provide targeted debt relief to address the financial harms of the pandemic, fulfilling the President’s campaign commitment; make the student loan system more manageable for current and future borrowers by cutting monthly payments in half for undergraduate loans and fixing the broken Public Service Loan Forgiveness (PSLF) program by proposing a rule that borrowers who have worked at a nonprofit, in the military, or in federal, state, tribal, or local government, receive appropriate credit toward loan forgiveness; protect future students and taxpayers by reducing the cost of college and holding schools accountable when they hike up prices.”

News of the president’s largess was met with mixed reviews.

The debt forgiveness is not absolute.

Those earning more than $125,000 and couples making more than $250,000 are not eligible.

Also not eligible are those who borrowed from private lenders.

As Biden admitted in his announcement:

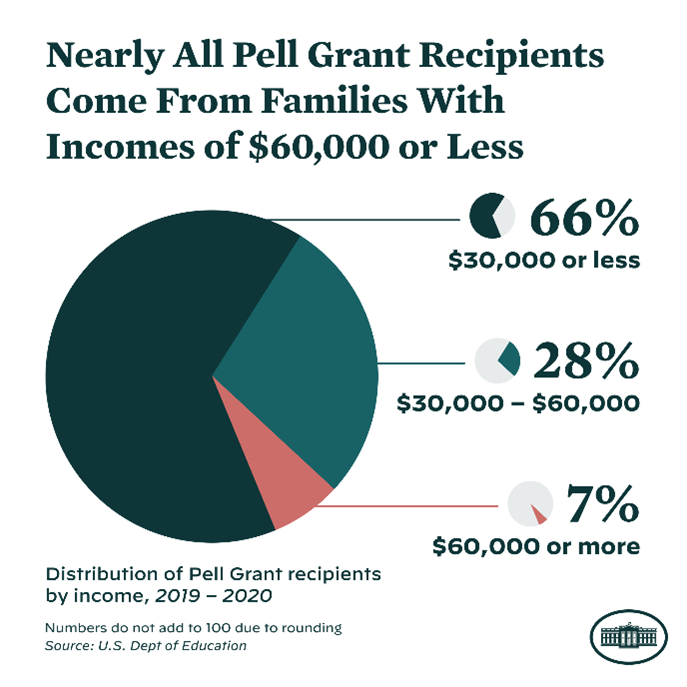

“Ninety-five percent of the borrowers can benefit from these actions. That’s 43 million people. Of the 43 million, over 60% are Pell Grant recipients. That’s 27 million people who will get $20,000 in debt relief. Nearly 45% can have their student debt fully canceled. That’s 20 million people who can start getting on with their lives.”

Even if it isn’t wiping the slate clean for all, 95 percent is astonishing, and it will do wonders for those who have been stymied in their attempts to fully participate in American society, who have been forced to delay starting families, businesses, buying homes, and have to work several jobs just to satisfy the banks holding borrowers’ financial futures hostage.

When campaigning for the presidency, Joe Biden stated:

“I propose to forgive all undergraduate tuition-related federal student debt from two- and four-year public colleges and universities for debt-holders earning up to $125,000, with appropriate phase-outs to avoid a cliff.”

Still riding the win from the passage of the Inflation Reduction Act, President Joe Biden scored another this week when he signed an executive order authorizing the federal government to cancel up to $20,000 in student debt.

While this frustratingly is not “all undergraduate tuition-related federal student debt” he promised when vying for the White House two years ago, it is nonetheless a major progressive move three months before one of the most consequential mid-term elections in the nation’s history.

There is lots of confusing minutia around this decision, and neither side is short on the inevitable punditry.

But, in short, here is what the student debt forgiveness plan entails, as Business Insider reported:

“Pell Grant recipients making under $125,000 a year will be eligible for up to $20,000 in debt relief.

“All other federal borrowers making under $125,000 a year can get up to $10,000 in loan forgiveness.”

Moreover, Biden paused loan repayment again “for the final time” one week before the looming deadline.

According to a White House fact sheet, the Department of Education will:

“Provide targeted debt relief to address the financial harms of the pandemic, fulfilling the President’s campaign commitment; make the student loan system more manageable for current and future borrowers by cutting monthly payments in half for undergraduate loans and fixing the broken Public Service Loan Forgiveness (PSLF) program by proposing a rule that borrowers who have worked at a nonprofit, in the military, or in federal, state, tribal, or local government, receive appropriate credit toward loan forgiveness; protect future students and taxpayers by reducing the cost of college and holding schools accountable when they hike up prices.”

News of the president’s largess was met with mixed reviews.

The debt forgiveness is not absolute.

Those earning more than $125,000 and couples making more than $250,000 are not eligible.

Also not eligible are those who borrowed from private lenders.

As Biden admitted in his announcement:

“Ninety-five percent of the borrowers can benefit from these actions. That’s 43 million people. Of the 43 million, over 60% are Pell Grant recipients. That’s 27 million people who will get $20,000 in debt relief. Nearly 45% can have their student debt fully canceled. That’s 20 million people who can start getting on with their lives.”

Even if it isn’t wiping the slate clean for all, 95 percent is astonishing, and it will do wonders for those who have been stymied in their attempts to fully participate in American society, who have been forced to delay starting families, businesses, buying homes, and have to work several jobs just to satisfy the banks holding borrowers’ financial futures hostage.

Image credit: US Dept. of Education

Republicans, are, naturally, apoplectic over “student debt socialism” (while gladly voting for massive tax breaks for their billionaire donors).

While borrowers can declare bankruptcy to relieve credit card and debt to healthcare providers, student loan debt is exempt, shackling 45 million Americans to a collective $1.6 trillion — the same amount republicans permanently cut for the economic royalists at the end of 2017 in the “Tax Cuts & Jobs Act”.

Three years ago, only 37% of student borrowers reduced their balances; 15% were in arrears or in default; almost half saw their balances grow.

University of Illinois College of Law bankruptcy expert, Robert Lawless (interesting name), explained:

“Congress has been tightening the screws on student loan discharge in bankruptcy for decades.”

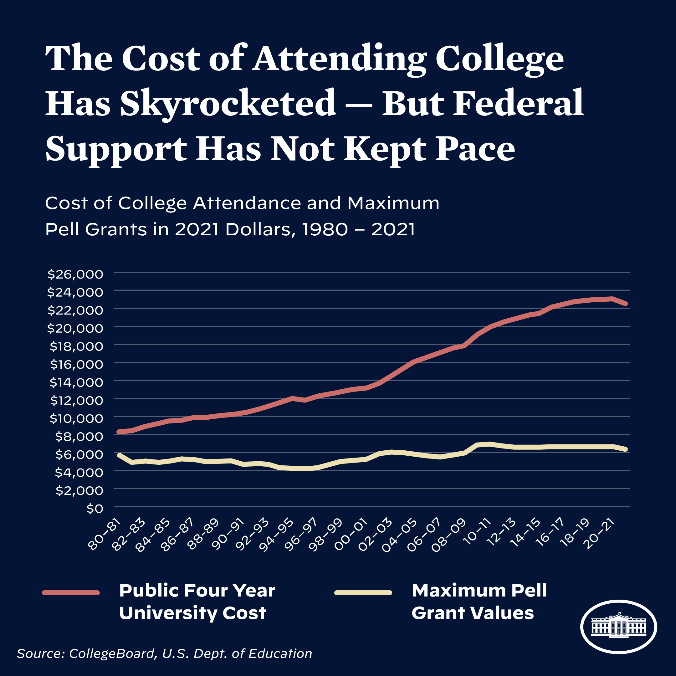

Image credit: College Board & US Dept. of Education

Congress began tightening the screws on student loan borrowers back in the late 1970s, around the time then-California Gov. Ronald Reagan ended tuition-free college in the California university system.

According to the Congressional Research Service, lawmakers claimed fearing student borrowers filing for bankruptcy after graduating, “and then enjoying a lifetime of income that education provides, but without the expense of paying back the loans.”

Up until the 1980s, when Reagan was elected president, tuition covered 20 percent of college; federal, state, and local subsidies covered the remaining 80 percent. Now it’s reversed, and with the Supreme Court approving a system of legalized political bribery, Wall Street banks make a killing on interest.

In 1998, legislation eliminated borrowers’ ability to discharge student debt if repayment presented an “undue hardship” and the loan had come due five years before filing for bankruptcy.

Massachusetts Sen. Elizabeth Warren, a bankruptcy expert, explained:

“One of the reasons that we have created this horrible situation with debt is that the bankruptcy laws were changed years ago to make it virtually impossible to discharge debts in bankruptcy.”

Up until now, President Biden refused to cancel student debt via executive order, stating Congress would have more legal authority.

Celebrating Biden’s executive order, Sen. Warren exclaimed, “Today is a day of joy and relief.”

True, but it’s only a start.

We can and must forgive all of it.

NAACP President Derrick Johnson commented, “Canceling just $10,000 of debt is like pouring a bucket of ice water on a forest fire.”

We are literally the only major industrialized nation that saddles students with mountains of debt.

Most countries send their students to college tuition free.

Denmark pays its students a $1,000 stipend to pursue higher education.

Why?

Because the government knows it is investing in its citizens’ intellectual capital.

An educated populace makes for a more productive, prosperous society, and people shouldn’t be punished for trying to be a part of it..

For every dollar we invest in a student’s higher education, we get back seven over that person’s lifetime in taxes.

That was part of the thinking behind the G.I. Bill.

Education, like healthcare, should be free.